ColorBlind/DigitalVision via Getty Images

Flushing Financial Corporation (NASDAQ:FFIC), founded in 1929 and headquartered in Uniondale, New York, is a commercial bank that primarily provides loans for multi-family real estate financing and commercial business loans.

With an attractive dividend yield and a significant discount to book value, the deal the market is offering seems to be a get-paid-to-wait one. In this post, I would like to expound on that after I provide some context regarding the business and recent results.

Business & Portfolio

This company operates a relatively small business that represents an equally small part of the industry. On December 31, 2023, Flushing had $8.5 billion worth of assets and currently trades around a market cap of $346 million.

The bank focuses on attracting retail client deposits and mainly allocating them to multifamily real estate credit through both origination and purchases of loans. To a lesser extent, it provides commercial business/mortgage loans, mixed-property mortgage loans, construction loans, and small business administration loans, among others.

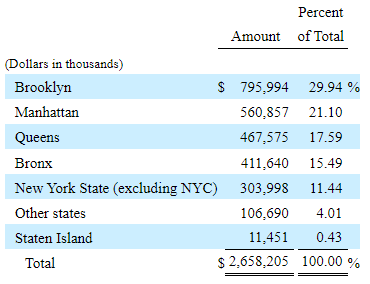

Regarding the market, Flushing provides its services through 27 offices which are spread across Brooklyn, Queens, Bronx, and Manhattan, among others. Note that most of its mortgages are backed by assets located in the NYC metropolitan area. Also, the loan portfolio has its highest concentration in Brooklyn:

10-K

Not surprisingly, the company faces a lot of competition as reflected by its total deposit market share of 0.35% in the markets in which it operates and the fact that it is the 23rd largest financial institution there.

To get a better idea of the loan portfolio’s composition, know that last time the company reported the allocation as follows:

-

Multi-family residential: 38.53%

-

Commercial real estate: 28.39%

-

Commercial business loans: 21.35%

Last, its requirements for originating a loan are pretty much standard: 125% debt service coverage ratio and 75% LTV. At year-end 2023, however, the average LTV ratio for the real estate segment was less than 36% and for NPLs backed by real estate, it was 34.1%.

Performance

At year-end 2023, deposits increased by 5% since the previous fiscal year while the loan portfolio witnessed a small decrease of almost 0.4%. Also, the average loan portfolio yield was 5.19%, a reflection of the increased interest rates as it was 4.35% the year before and 4.13% in 2021. However, net interest spread narrowed to 1.72%, down from 2.92% the year before and 3.14% in 2021. At the same time, NIM decreased to 2.24% in 2023, down from 3.11% the year before and 3.24% in 2021, also indicating a significant liability sensitivity.

Moving to profitability, revenue reached $401.4 million in 2023, a 26.79% YoY increase. Unsurprisingly, net interest fell by 29.3% to $168.6 million. It’s worth noting that non-interest income keeps making new highs; it climbed to $22.6 million in 2023, up from $10 million the year before and $3.6 million in 2021.

But predictably, net income declined. It went down by 62.7% to $28.6 million. Similarly, EPS decreased by 61.6% to $0.96. Tangible book value saw a slight increase of 1% to $22.54 per share. Last, ROAA for the fourth quarter of 2023 came at 0.38%, 10 bps lower on a YoY basis, and ROAE was at 4.84%, down from 6.06% in the same quarter the previous year.

Now, management has recently shared that it expects core NIM to experience further pressure and fall below 2.15% in the short term as the repricing of CD funds will exceed the repricing of loans. However, it also expects that by the middle of 2024 the loan repricing will exceed liability repricing.

The CEO, John Buran said this in the last earnings call concerning the liability sensitivity:

I don’t think we’re looking to reduce it any further. And obviously, the market hasn’t done such a great job of predicting the number of rate cuts or increases. So given the fact that historically our balance sheet had a heavy liability sensitivity, it still does today at its core basis. So I think that we have options to increase the liability sensitivity in the balance sheet should we see some certainty with respect to the Fed moves, and we’re exploring those options. So we haven’t made any decisions as to the timing and magnitude of rate cuts at this point in time, and we’re watching very carefully what’s happening in the market. We’ve been disappointed before in terms of the Fed making cuts. So we wanted to position ourselves to be successful in either environment.

I appreciate the conservative stance because I have started resisting placing too much faith in potential cuts. This stance is also reflected in the mention of the $325 million of swaps which mature in 2025. In the CEO’s own words:

we’re going to have a bigger opportunity in 2025 to manage asset versus liability sensitivity, because we do have a fair number of swaps coming off.

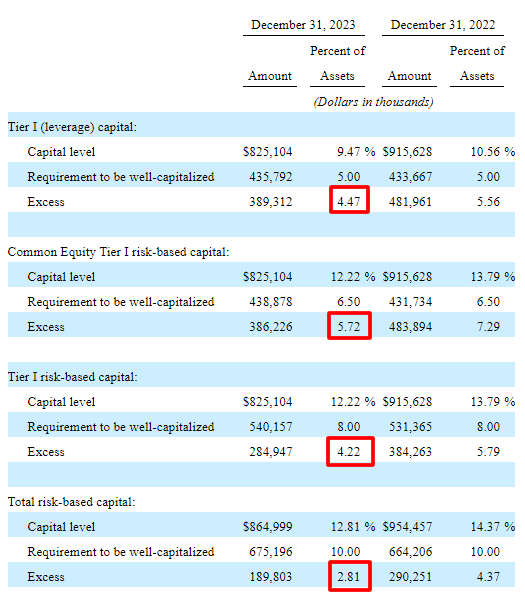

Solvency & Liquidity

On the leverage front, Flushing doesn’t operate using too much. Its Tier 1 leverage ratio is well above the regulatory minimum. The same thing applies to capital requirements concerning the most liquid assets (common equity Tier 1) and total risk-based capital, as you can see below:

10-K

All in all, the company seems to be more than well-capitalized.

As for the cost of its liabilities, in 2023 deposits averaged a 3.19% interest rate and its wholesale funds 3.29%. While deposit costs don’t appear to be too high, we have to note that only 12.52% of them are non-interest-bearing. On the bright side, this allows for a more stable base, which kind of alleviates the lack of a margin of safety observed in its current LDR of 101%. Its liquidity growth also helps here as cash increased by 13.44% in 2023 since 2022 to $172.1 million.

Now, the potential deterioration of the loan portfolio doesn’t appear to be very alarming, even today. At year-end 2023, 2.96% of it was rated as “Watch”, 0.29% as “Special Mention”, 0.77% as “Substandard”, and 0.06% was classified as “Doubtful”. Additionally, NPLs represented 0.36% of total loans, 11 bps lower than in 2022. Last, the reserve coverage ratio was 0.58% (steady on a YoY basis) and the net charge-off ratio was 0.16% for the year 2023 (0.02% in 2022).

Dividend & Valuation

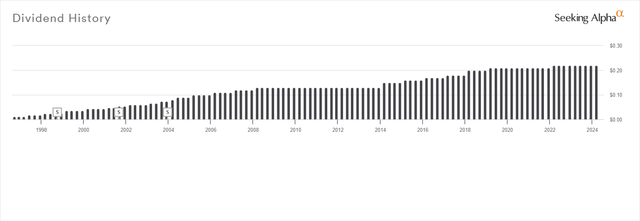

FFIC currently pays a quarterly dividend of $0.22 per share, resulting in a dividend yield of 7.38%. This is a very decent yield right now, and though the payout ratio is currently at 91.66% based on 2023 results, the company hasn’t cut or suspended the distribution for a very long time. Quite the contrary actually:

Seeking Alpha

Still, a cut shouldn’t be off the table if interest rates rise further; while I am not optimistic about rate cuts right now, I believe that further rate hikes seem to be unnecessary.

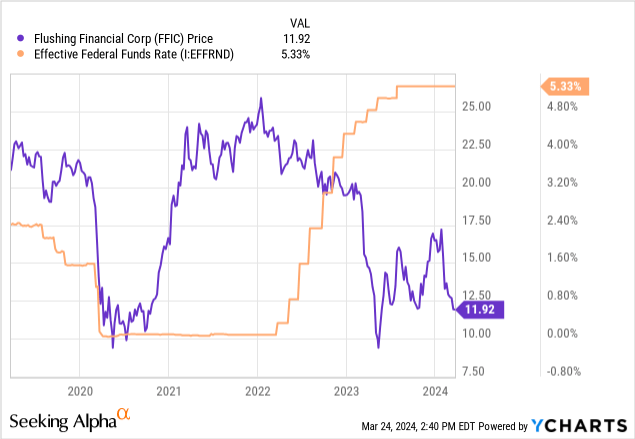

Predictably, the market appears to have responded to the hikes starting in 2022 by pushing the price of FFIC to 2020 levels:

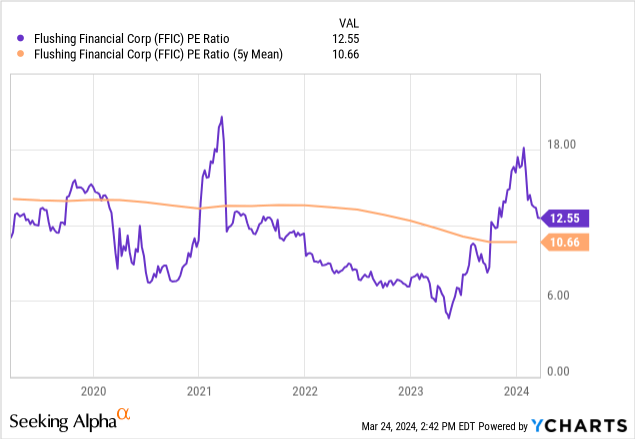

If the Fed Funds rate starts decreasing, share demand could increase but I doubt we will see pre-hike levels very soon as this will probably happen slowly and near-zero interest rates are unlikely in the short to medium term. Another thing I should note is that the stock is trading close to its 5y mean earnings multiple:

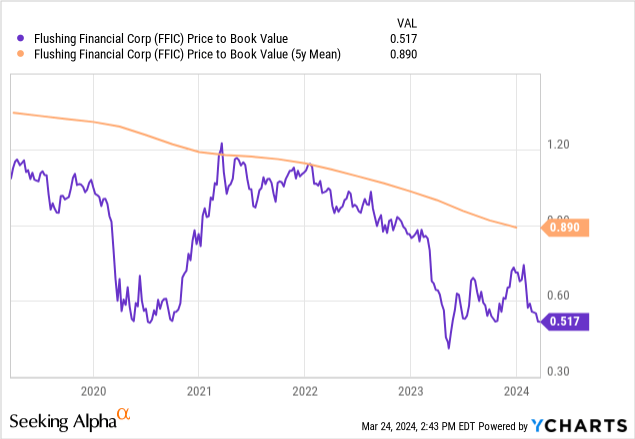

Considering the degree to which EPS shrank in 2023, this isn’t surprising. But as credit quality seems to be stable, the difference between the current PB ratio and the 5y mean one suggests a much larger upside:

Risks

A Flushing-specific risk we should note is a potential dividend cut or suspension. Though it hasn’t happened before, there is a first time for everything. Regardless, I find myself justified in downplaying this risk as I don’t see a high probability of further interest rate increases. And it seems that if management intends to preserve the reputation of FFIC as a decent dividend pick, the business has adequate liquidity to maintain it even in the event of more pressure on its profitability for some time.

Beyond that, I don’t see an immediate risk for the stock price here. You should know that all the general risks that similar enterprises face in the industry apply, such as interest rate risk, credit risk, and regulatory risk; so it’s good for shareholders to monitor those too.

Verdict

All in all, there is a significant margin of safety provided by the discount to book value which in turn doesn’t seem justified considering the most significant aspects of the business. Also, the dividend is the cherry on top and can significantly reduce a potential opportunity cost, as well as allow shareholders to be patient. I must therefore rate FFIC a strong buy at current levels.

What’s your opinion? Do you own the stock or intend to? What are your thoughts on the attractiveness of this opportunity if you deem it as such and what are your worries? Let me know below and I’ll get back to you soon. Thank you for reading.